(Bloomberg) – The highest elections in Germany for years pave the way to an increase in spending, the markets predicting the end of an era for limited fiscal policy.

Most of Bloomberg

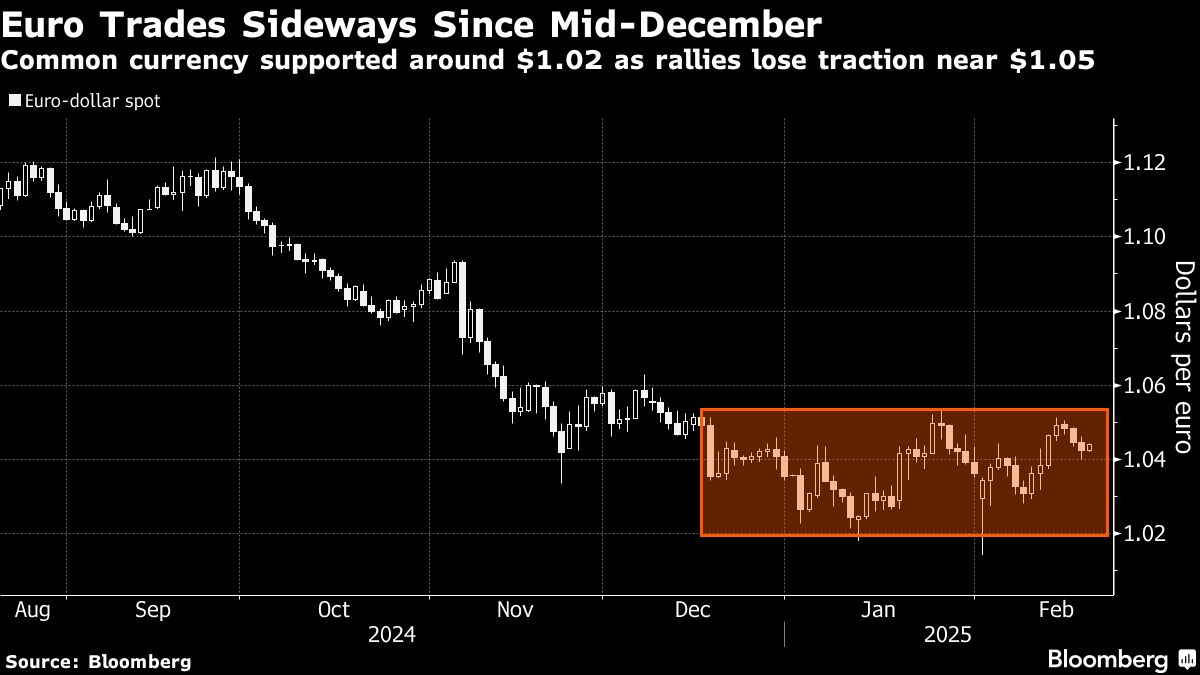

The euro increased by 0.3% to almost $ 1.05 in Asia after exit surveys and early voting projections have shown that the conservative block led by Friedrich Merz winning on Sunday, in accordance with ‘expected. Obligations and term contracts on shares are starting to negotiate at 1 hour in Berlin.

“For the markets, the result is favorable because Germany will always have a centrist government, but it will rotate a more pro-enterprise and pro-investment orientation,” said Matt Gertken, chief geopolitical strategist of BCA Research. The nation “will also be likely to avoid a massive split with the Trump administration on trade, Russia or China”.

The CDU / CSU block of Merz should win with 28.9% of the votes, before the party on the far right of the AFD and the social democrats of Chancellor Olaf Scholz. Speaking on Sunday evening, Merz said that he wanted to form a new government as soon as possible, noting that the world “would not wait for us” for the long talks of the coalition.

In the best of cases for markets, Merz would form a strong coalition with one or two other traditional parts. Such a result would probably facilitate the way to reforms that could restart the Moribonde economy of Germany – and allow modifications to a constitutional borrowing limit, introduced in 2009 and known as the debt braking.

For Krishna Guha, Vice-President of Evercore Isii, a bipartite coalition with the CDU / CSU and the SPD and enough potential support of other parties to reform the brake would be “the best result available for Europe, Ukraine and the financial markets ”.

This would mark a Seachange for Germany, which has long preached budgetary prudence. But with the United States that push Europe to spend more in defense, such a change is now on the table.

Admittedly, with the votes which are still counted on Sunday evening, it was not luxurious if the minority parties would accumulate enough votes to obtain more than a third of the seats in Parliament. This could allow them to block constitutional changes, potentially arousing market volatility.

The assets began to assess the prospect of a result that supports additional loans: German obligations have slipped from key references, more dated titles falling more than those who have shorter deadlines, pushing the yield curve to Its stiff since 2022. It is because the additional loan is additional additional loan. tends to weigh more on the longer tenors.

Meanwhile, the country’s reference gauge of the country’s equity prices has reached a record level – pulled in part by a 45% rally this year by Rheinmetall AG, the only pure -game defense actions of the index.

Companies in the defense sector are about to benefit from any budgetary reform that releases capital for more investment in the European army. These actions have already been in tears this year, with Citigroup analysts Inc. noting before a rally last week which increased defense spending to 2.5% of GDP, against 2%, would increase the capital assessments of these companies 15 to 20%.

The euro also benefited from the entries of German shares this year and was on the right track to gain almost 1% in February, its best monthly performance since August. Data from Depository Trust & Clearing Corporation show that 60% of the options placed this year to expire Monday targets a stronger euro. It is despite a broader concern that the currency could ultimately undergo parity with the dollar this year.

“The euro was bogged down by structural weakness in Germany, which should take a tour of the best if the new government follows with the reforms and plays a more active role in infrastructure and defense,” said Dane Cekov, Macro Senior and the FX strategist on the Satchbank 1 AS markets. “However, this electoral result will not change the situation for the euro, because the incoming prices of Trump will harm the Euro to come.”

A large part of the long -term trajectory of the common currency also depends on whether investors think that the US dollar has culminated. Speculative merchants, including hedge funds and asset managers, have reduced their bets on other dollars gains for a fifth consecutive week until February 18, according to data from the ComboDity Futures Trading Commission.

However, there are signs that German politicians, including Merz, recognize the need for greater borrowing – although in one of his last points to voters on Friday, he said that restrictions on loan of the government “are not a priority”. Germany has the capacity to borrow more, with some of the lowest costs and the smallest piles of debts in the euro zone.

The issues at the national level are also high. The German economy decreased in 2024 for a second consecutive year, the second time that this has happened since 1950. Years of underinvestment, the loss of cheap Russian gas and a long -standing collapse in China – a Partner of key trading – have weighed on production, causing a long time the search for soul on how Germany can revive growth.

“There is not much room for disappointment on the stock markets at the moment, and in the short term, this could be positive,” said Neil Birrell, director of investments at first Miton Investors.

– With the help of inside Macdonogh, Vassilis Karamanis, IRA Iosebashvili, Allegra Catelli, Sagarika Jalinghani and Matthew Burgess.

(Updates with additional comments, context everywhere.)